DIY-Garden Network: Report of the second half of 2025 (part 2)

The following section presents the second installment of the 2025 Italian DIY-garden monitoring, focusing on brand affiliations, store formats, and retail chains.

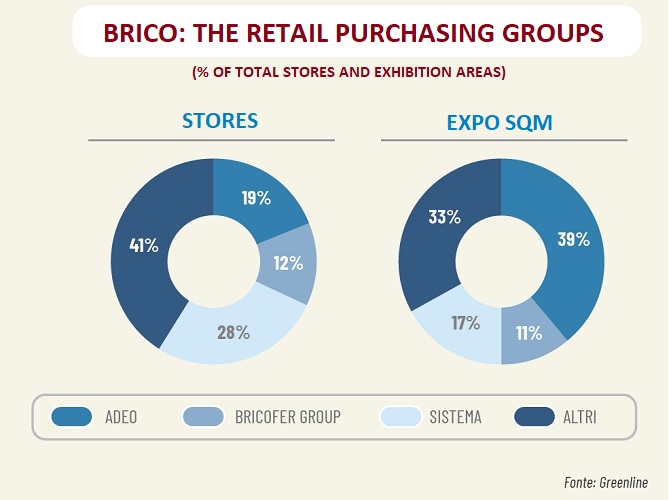

AFFILIATION

The world of affiliation and trade associations in the Italian market primarily consists of two models: franchising and affiliation proposals offered by large distribution groups, and cooperatives or voluntary unions made up of independent entrepreneurs who team up to form buying groups. In our analysis, we define ‘company-owned stores’ as those owned by the distribution group, and ‘affiliated centers’ as those that participate in association, affiliation, or cooperative models.

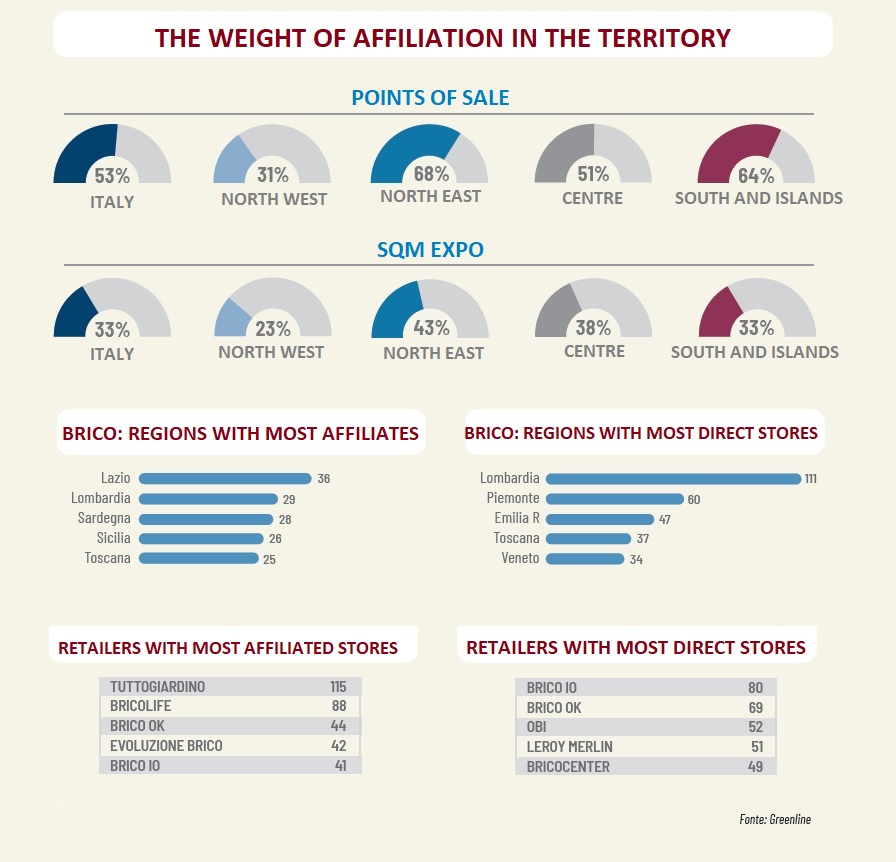

Directly-operated stores—those owned by the distribution group—account for 47% of Italian stores in 2025, an increase from 46% at the end of 2024. This figure rises to 69% in the North-West, while remaining below 50% in other macro-regions. However, when analyzing sales floor area, the situation is reversed, as directly-operated stores are generally larger than affiliated ones. In fact, affiliated stores represent “only” 33% of the total exhibition space, down from 34% at the end of 2024. The North-East is the region where affiliation is most significant, accounting for 43% of the total floor space. In contrast, the North-West sees only 23% of its floor space managed through affiliates.

Since garden center chains are almost entirely composed of stores affiliated with consortia or franchising schemes, we have extracted data specifically for DIY centers. In this sector, the percentage of directly-operated stores rises to 59%, accounting for 76% of the total exhibition area. The share of direct stores increases significantly in the North-West, reaching 78% (representing 88% of floor space), and in the North-East with 61% (72.9% of floor space). Conversely, figures fall below the national average in Central Italy (52% of stores and 67.5% of floor space) and the South & Islands region (39% of points of sale and 69.5% of floor space).

The regions with the highest number of franchised DIY centers are: Lazio (36 stores), Lombardy (29), Sardinia (28), Sicily (26), and Tuscany (25). Together, they account for 144 stores, representing 47% of all franchised DIY centers. Conversely, the regions with the highest number of directly-managed DIY centers are Lombardy (111 stores), Piedmont (60), Emilia (47), Tuscany (37), and Veneto (34). These regions account for 289 stores, or 64.5% of all directly-managed DIY centers in Italy.

Considering the entire panel of DIY and garden centers, the chain with the largest number of directly-managed stores is Brico io with 80 locations, followed by Brico Ok (69), Obi (52), Leroy Merlin (51), and Bricocenter (49).

Keep notice. To better understand the text, it is important to keep in mind that Italy is conventionally divided into 4 macro-areas:

- The North West: Aosta Valley, Piedmont, Liguria, Lombardy

- The North East: Trentino-South Tyrol, Veneto, Friuli Venezia Giulia, Emilia-Romagna

- The Center: Tuscany, Umbria, Marche, Abruzzo, Lazio

- The South and Islands: Molise, Campania, Apulia, Basilicata, Calabria, Sicily, Sardinia

HOW FORMATS ARE CHANGING

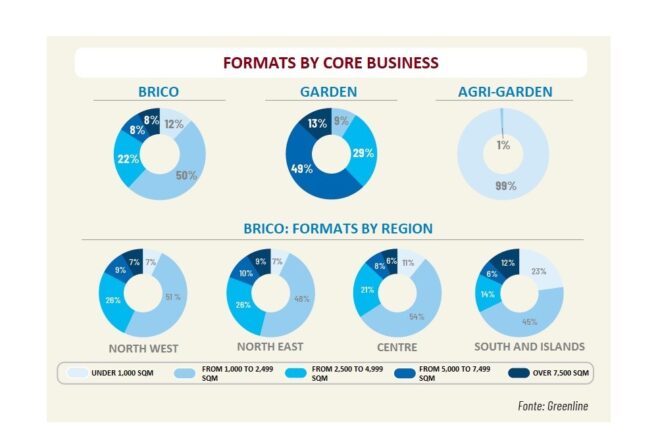

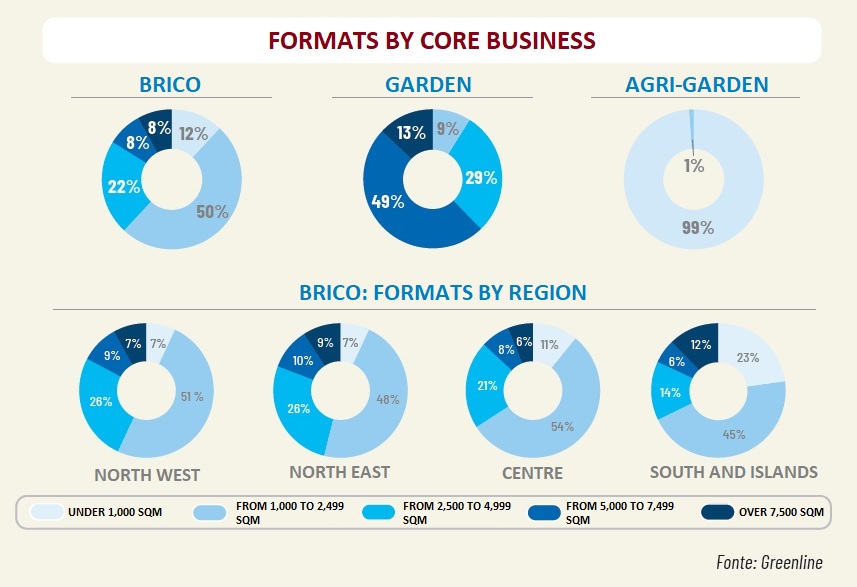

To meet the needs of the modern customer, retail formats have also evolved. Alongside large-scale stores exceeding 5,000–7,000 sqm, smaller formats have been developed that are better suited for neighborhood retail. Naturally, the type of product offering also plays a significant role. Garden centers, which often originate from nurseries, can rely on greenhouses and vast outdoor spaces: 62% of them have a surface area larger than 5,000 sqm. In contrast, agri-garden centers—often an evolution of traditional agricultural supply stores—feature more compact dimensions. DIY centers sit in the middle, with only 16% exceeding 5,000 sqm. Half of them (50%) have a footprint between 1,000 and 2,500 sqm, while 22% occupy an area between 2,500 and 5,000 sqm.

Looking more closely at DIY centers, which are the most numerous in terms of volume, we find that small-scale stores (under 1,000 sqm) are more prevalent in the southern regions: they represent 23% of all DIY centers in that macro-area.

Conversely, the area with the highest concentration of stores exceeding 5,000 sqm is the North-East, accounting for 19% of the total DIY centers.

DIY centers located in cities are generally larger than those in peripheral municipalities: they have an average floor space of 3,460 sqm, compared to 2,719 sqm for provincial stores and a national average of 2,907 sqm.

Significant differences in format also emerge when comparing directly-managed DIY centers with franchised (affiliated) ones. Compared to the national average of 2,907 sqm, directly-managed stores increase to an average of 3,714 sqm.

CHAINS IN 2025

Even though we noted that the total number of stores is decreasing, this does not mean there were no new openings in 2025. In fact, the final figure represents the net balance between new openings and closures—whether permanent or resulting from the termination of franchising agreements.

First and foremost, Tecnomat, Brico io, and the Garden Team consortium deserve a mention, as they were the only distribution groups to expand their total store network.

In 2025, Tecnomat opened 3 new stores: in Sassari on March 12, in Palermo on November 19, and in Bari on December 19. The chain was already present in Sassari, so this was a relocation: the new store opened in 2025 replaced the previous one opened in 2010, moving to a larger and more functional site about 1 km away. Brico io was also particularly active in 2025 with 3 new openings: 2 franchisees in Vignanello (VT) and Varese, and 1 directly operated store in San Giorgio di Piano (BO).

The Garden Team garden center consortium, meanwhile, welcomed two Nicora Garden stores in Varese, which left Giardinia. Giardinia also completed two new openings in 2025: a new franchisee, Pet Garden in Leporano (TA), and a new garden center in Castiglion Fiorentino by the already-affiliated, Segantini Green Passion.

Bricocenter opened a new franchised store in Siena and a directly operated store in Benevento. At the same time, it worked on the restyling of the four stores acquired from Self in 2024, located in Vercelli, Asti, Alba (CN), and Borgo San Dalmazzo (CN).

In 2025, Leroy Merlin opened stores in Salerno and San Giovanni La Punta (CT). The latter was a relocation and expansion, coinciding with the closure of the Catania Fontanarossa store that had opened in 2022. The company also renovated its Rozzano and Carugate stores, which led to the simultaneous closure of the Assago and Caponago centers. In 2026, it will close the Baranzate store and open a new one in Arese.

Thanks to its new member, Gs Distribuzione, Evoluzione Brico has opened two new stores in the Abruzzo region (Chieti province), specifically in Rocca San Giovanni and Lanciano.

METHODOLOGY OF THE SURVEY

The ‘Gds Brico-Garden Monitoring’ is a semi-annual survey that the author has conducted continuously since 1988. To analyze the evolution of organized retail formats specializing in DIY and gardening within Italy, we selected Large-Scale Specialized Retail brands and Buying Groups (consortia, voluntary unions, etc.) that meet two primary criteria: a presence of at least three points of sale and a propensity for development—defined as the systematic opening of new stores, whether company-owned (direct) or franchised.

The display areas indicated refer to indoor sales floor space; therefore, parking lots, offices, and warehouses are excluded.

By ‘company-owned stores’, we mean outlets owned directly by the retail group; by ‘franchised stores’ (or ‘affiliates’), we mean outlets owned by private entrepreneurs who participate in organized retail formats (such as franchising) or are affiliated with buying groups and consortia.

All data are provided by the retailers themselves and processed by the author. In the rare instances where estimates are used, they are always specified in the charts.